Nashville merchants face a fast-changing mix of processing costs, card-brand rules, state regulations, and compliance requirements. If you run a boutique in 12South, a café in Germantown, a honky-tonk on Lower Broadway, or a home-services company serving Davidson County, mastering credit card fees isn’t optional—it’s a profit lever.

This updated guide explains every major fee, how they’re calculated, the latest rule changes, Tennessee-specific considerations, and practical ways to lower your effective cost of acceptance.

Throughout, you’ll see terms Nashville merchants actually encounter—interchange, assessments, PCI DSS 4.0, surcharging, convenience fees, chargebacks, and more—plus clear steps to make fees predictable and manageable.

Why credit card fees matter in Nashville’s local economy

For many Nashville merchants, card payments represent 70–95% of sales volume, which means a small improvement in effective rate can exceed your monthly rent or payroll burden. Margins in hospitality, retail, and service businesses are already squeezed by higher input costs and rising wages.

Add in Nashville’s relatively high combined sales tax—commonly 9.75% for most transactions in the city—and every basis point counts when you’re setting prices, forecasting cash flow, or deciding whether to launch a new product line.

Knowing what drives credit card fees for Nashville merchants helps you avoid blanket price hikes that could dampen demand or hurt local competitiveness.

Credit card fees also influence strategy. If your mix includes many small tickets (coffee, pastries, quick-serve items), per-item costs and debit optimization matter more than headline percentage rates.

If you’re B2B or sell higher-ticket goods (instruments, custom furniture, medical aesthetics), Level 2/3 data and interchange optimization can move the needle.

Nashville merchants increasingly use omnichannel sales—POS in-store, keyed invoices, links, and eCommerce—so it’s important to understand how each channel affects cost, risk, and dispute exposure. Getting this right turns processing from a “cost center” into a controllable operating expense.

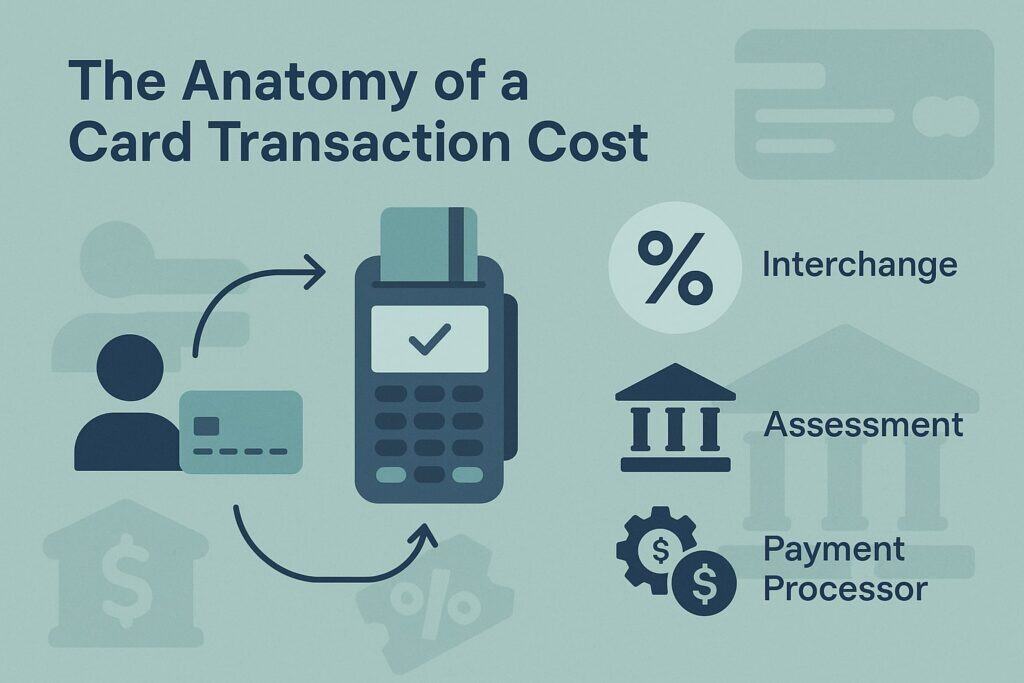

The anatomy of a card transaction cost

At a high level, you’ll see three components in most statements: interchange, assessments, and your processor’s markup. Understanding these building blocks helps Nashville merchants audit their statements and negotiate confidently.

Interchange: the base cost you don’t control—yet you can influence

Interchange is paid to the card-issuing bank and is the largest slice of credit card fees for Nashville merchants. Rates vary by card type (credit vs debit), product (rewards, corporate, business), entry method (chip, contactless, keyed), data quality, and industry category.

You don’t “set” interchange, but you can influence which interchange category your transactions qualify for by capturing the right data, using chip/contactless, batching on time, and choosing the best routing for debit.

For debit, the Durbin Amendment (Regulation II) caps interchange for large issuers (assets ≥$10B), while exempting small issuers. The Federal Reserve proposed revising the cap, which—if adopted—would lower certain covered-issuer debit fees and require biannual updates.

That matters because Nashville merchants often run heavy debit volumes in QSR, grocery, and convenience segments. Keeping terminals configured for proper debit routing and accepting PIN when it makes sense can materially reduce your blended cost of acceptance.

Card-brand assessments: small percentages that add up

Assessments are the network fees paid to the card brands (Visa, Mastercard, AmEx, Discover). They’re typically fractions of a percent plus tiny per-item charges. Assessments don’t usually make headlines, but they add meaningful basis points to your effective rate, especially at scale.

Because assessments are brand-set and relatively uniform, the lever for Nashville merchants is managing card mix and avoiding unnecessary downgrades that can layer on extra network charges.

Processor markup: the part you can negotiate

Your markup is the processor/ISO/MSP’s revenue for gateway, risk management, support, and service. Markup can be priced as:

- Interchange-Plus (cost-plus): a transparent % + per-item over interchange/assessments.

- Tiered/Bundled: qualified/mid/non-qualified buckets, harder to audit.

- Flat-rate: simple headline pricing, sometimes hiding higher costs for certain transaction types.

- Membership/subscription: fixed monthly plus tiny cost-plus variable fees.

For most established Nashville merchants, interchange-plus or a well-designed membership model provides the best visibility. Always request a full fee schedule, gateway fees, chargeback costs, PCI program fees, monthly minimums, and basis-point markups. Then benchmark your effective rate by channel—card-present, eCom, invoicing—and by card type.

Debit vs. credit in 2025: what Nashville merchants should prioritize

Debit and credit behave differently in both cost and risk. Debit from covered issuers is subject to Regulation II’s cap structure, while exempt debit can cost more. When volume skews to small tickets, optimizing for debit can drive savings.

For higher-ticket or B2B, credit may dominate, and the interchange game shifts to data quality and correct category qualification. In late 2023, the Fed proposed revisions to Regulation II’s debit cap formula, moving to a lower cents-plus-percent structure with periodic adjustments.

While proposals aren’t final until adopted, merchants should prepare by ensuring terminals, gateways, and routing logic can support network choice and PIN where appropriate.

Credit acceptance remains essential for consumer financing and rewards-driven spend—just remember that rewards often carry higher interchange, so capturing AVS/CVV, using chip, and minimizing key-entry downgrades helps offset those costs.

Surcharging, cash discounting, and convenience fees in Tennessee

Surcharging and convenience fees are often confused, yet the rules differ by network, state law, and transaction flow. Tennessee allows credit card surcharges (not on debit or prepaid), provided you follow card-brand rules and consumer-protection requirements.

Nashville merchants considering a program must distinguish among three models to stay compliant and protect customer trust.

Is surcharging legal for Nashville merchants?

Yes—Tennessee permits credit card surcharges as of 2025, subject to card-brand rules and disclosure requirements. There’s no extra Nashville-specific prohibition; however, you must comply with network caps, signage, receipt disclosures, and not surcharge debit or prepaid—even if a customer “runs debit as credit.”

If you sell into states where surcharging is restricted, be sure your eCommerce or mail/phone order setups can suppress surcharges based on the card’s BIN and billing address.

Card-brand caps and what they mean in practice

As of the most recent updates, Visa caps surcharges at the lower of your actual merchant discount rate or 3%, while Mastercard caps at 4% (again, the lower of your cost of acceptance or the brand cap).

American Express and Discover generally align at up to 4%, with similar cost-of-acceptance limitations. You must apply the fee only to credit, disclose it clearly at the point of entry and on the receipt, and ensure you’re not profiting from the surcharge.

Brand-level or product-level surcharging is allowed within the networks’ rules, but you cannot apply different fees in a way that discriminates unlawfully among consumer segments.

Implementation checklist for Nashville merchants

Before launching surcharging, Nashville merchants should:

- Notify your acquirer in advance (Visa removed the direct network notification; confirm with your processor).

- Configure POS/gateway to automatically detect card type and suppress fees on debit/prepaid.

- Post signage at the entrance and point of sale explaining the surcharge and that it applies to credit only.

- Line-item the surcharge on receipts with compliant naming.

- Test omnichannel: terminals, eCommerce, and invoices must apply rules consistently.

- Set the right percentage: the lower of your merchant discount rate or the brand maximum.

- Train staff to answer consumer questions politely and accurately.

Following these steps reduces the risk of fines or forced refunds during brand audits or mystery shops.

PCI DSS 4.0: compliance requirements that impact your cost of acceptance

Security compliance affects both your risk and your fees. PCI DSS 4.0 replaces 3.2.1, with December 31, 2024 as the retirement of 3.2.1 and March 31, 2025 as a key date when many future-dated 4.0 requirements become effective.

For Nashville merchants, the shift means updating SAQs, strengthening MFA and password policies, reviewing encryption and segmentation, and ensuring service providers (gateways, POS vendors) attest to 4.0 readiness. Non-compliance can mean monthly PCI program fees, higher risk exposure, and potential fines after a breach.

Practical tips: keep card data out of scope using P2PE or validated semi-integrated terminals, tokenize online payments, and rotate keys and passwords per 4.0 guidance.

For multi-location Nashville merchants, centralize compliance evidence and calendar critical dates so renewals don’t lapse. Ask your MSP for an updated 4.0-aligned SAQ wizard and ensure your QSA, if used, understands your exact environment—card-present, eCom, or both.

Local tax context: how Nashville’s sales tax interacts with payment fees

While processing fees are separate from sales tax, they influence your pricing strategy for tax-inclusive or tax-exclusive displays. Nashville’s widely referenced combined rate is 9.75% for many transactions, made up of a 7% Tennessee state rate plus a local add-on in Davidson County.

Merchants should ensure surcharges, if applied, are not taxed improperly—work with your tax advisor or POS provider to configure surcharge lines correctly so you don’t over-collect or under-remit. Also monitor any local ballot measures or transit-related sales tax changes that may affect your receipts and customer price perception.

If you sell across nearby jurisdictions (Belle Meade, Berry Hill, Forest Hills), rates can differ slightly from Nashville’s headline rate. Keep your POS zip-sensitive to avoid mis-applied tax, especially for delivery. Periodically verify rates against a trusted tax service.

Proven strategies to reduce the effective cost of acceptance

Even though interchange and assessments are “set,” Nashville merchants have many levers to lower overall costs while maintaining a great checkout experience.

Optimize debit routing and encourage true debit

Enable network routing so regulated debit runs the least-cost rail, and keep terminals set to favor chip/PIN when appropriate. Post friendly prompts like “Debit? Save time with tap or chip PIN” for small-ticket businesses.

Ensure your gateway supports least-cost debit routing online, too. These moves help Nashville merchants trim basis points without hurting customer satisfaction.

Capture Level 2/3 data for B2B and higher-ticket categories

If you sell to businesses or accept corporate/purchasing cards, configure your gateway to send tax amount, customer code, and other L2/L3 fields. Doing so can qualify transactions for lower interchange categories, reducing costs on every eligible sale.

Many Nashville merchants in wholesale, medical/dental, industrial supply, and professional services overlook this and leave savings on the table.

Reduce downgrades with clean transactions

Use chip/contactless rather than magstripe, batch daily before the cutoff, and avoid unnecessary key-entry. Add AVS and CVV checks for card-not-present. Each of these reduces interchange downgrades and risk flags that can push transactions into more expensive categories.

Right-size your pricing model

If your mix is heavy in small tickets, a plan with lower per-item charges might beat a low percentage. If your tickets are larger, basis-point markups matter more. Ask for interchange-plus quotes and compare a recent month using exact card mix and channels.

Then negotiate on the variables that actually drive your spend: auth fees, gateway fees, AVS fees, and chargeback fees—not just the headline discount rate.

Minimize chargebacks and represent effectively

Disputes raise both direct losses and indirect costs (higher risk, reserve holds). Adopt clear descriptors, fast digital receipts, and consistent refund policies.

For hospitality and events near Broadway and the Gulch—where traveler spend is high—enable cardholder verification steps for large tabs and consider text-to-pay invoices with verified links.

Working with a transparent processor or MSP in Nashville

When evaluating providers, require a complete pricing schedule and a sample statement in your exact configuration (same POS, same card-present vs online mix). Ask for:

- Interchange-plus markup (basis points + per-item) and all fixed fees.

- Gateway and tokenization fees.

- PCI program fees and how they change under PCI DSS 4.0.

- Chargeback management costs and representation support.

- Contract term, early termination, and equipment ownership.

- Support SLAs for weekend/late-night hospitality service calls.

Request a written surcharge or cash-discount compliance checklist if you plan to pass fees, aligned to Visa/Mastercard caps (3% for Visa; up to 4% for others, or your cost—whichever is lower), plus signage and receipt language examples. Verify your acquirer notification process and ensure your POS/gateway can block fees on debit and prepaid.

Example cost scenarios for Nashville merchants

These illustrations show how small configuration changes can alter effective cost. They’re examples only—use your own statements to model outcomes.

Neighborhood coffee shop, average ticket $7

Volume is mostly regulated debit plus some rewards credit. Prioritize low per-item fees and strong debit routing. Chip/contactless speeds lines and reduces downgrades. A surcharge may frustrate frequent local customers; consider cash discount only if you can execute cleanly and compliantly without confusing signage.

Boutique retailer in 12South, average ticket $85

The mix includes rewards, credit and some debit. Interchange-plus with modest per-item fees often beats flat-rate. Use address verification for eCom orders and capture emails at POS for digital receipts to fight friendly fraud.

If you explore surcharging, cap it correctly and disclose clearly at the entrance and at checkout; test customer sentiment first.

B2B services firm, average ticket $1,200

Corporate cards dominate. Configure Level 2/3 data and ensure invoices include tax and PO fields so the gateway can pass everything required. This change alone can reduce effective rates by dozens of basis points on qualifying transactions.

FAQs

Q1) What’s the difference between a surcharge, a cash discount, and a convenience fee?

Answer: A surcharge is an added fee for using a credit card; it can’t be applied to debit or prepaid and must follow brand caps and disclosure rules. A cash discount lowers the posted price for cash and keeps the card price as the regular price—executed properly, it isn’t a surcharge.

A convenience fee is a flat fee for using an alternative channel (like paying by phone or online) and has very specific brand rules; not all scenarios qualify. Tennessee permits surcharging with proper compliance, but the card networks’ rules still govern caps and how/when you can apply it.

Q2) What are the current surcharge caps I should know?

Answer: Visa caps surcharges at the lesser of your actual merchant discount rate or 3%. Mastercard allows up to 4% (again, not above your actual cost).

American Express and Discover generally allow up to 4%, subject to cost-of-acceptance and disclosure rules. None of the brands allow surcharging debit or prepaid, even when a customer selects “credit.” Always verify your POS/gateway blocks fees on debit BINs.

Q3) Do I need to notify anyone before I start surcharging?

Answer: You must notify your acquirer/processor and implement required signage and receipt disclosures. Visa previously required network notice but changed that process; processors still expect 30-day lead time and proof of compliant setup. Work with your MSP to ensure brand-compliant wording and placement.

Q4) How does PCI DSS 4.0 change my obligations?

Answer: PCI DSS 4.0 introduces stronger authentication, expanded testing, and clearer roles for service providers. Key dates include 3.2.1 retirement at Dec 31, 2024, and future-dated 4.0 controls effective March 31, 2025.

Many Nashville merchants can reduce scope by using P2PE devices, tokenized eCom, and semi-integrated POS. Ask your vendor for 4.0-aligned SAQs and evidence.

Q5) What about debit fees under the Durbin Amendment—can I lower those?

Answer: Covered-issuer debit (big banks) has a capped cents-plus-percent framework; exempt debit (small issuers) can be higher. The Fed proposed lowering caps and reviewing them regularly.

Your best move is to enable least-cost routing and support PIN where it fits your checkout. These steps help Nashville merchants reduce debit costs today and adapt easily if the proposal becomes final.

Q6) Are surcharges taxed in Nashville?

Answer: Sales tax rules apply to taxable sales of goods/services; whether a surcharge line is taxable can depend on configuration and item taxability.

Many POS systems treat the surcharge as part of the taxable selling price if the underlying item is taxable—others do not. Because Nashville’s combined rate often sits at 9.75%, verify your setup with your POS and advisor to avoid under- or over-collection.

Q7) Will surcharging alienate my customers?

Answer: It can—especially for frequent small-ticket purchases. Consider piloting surcharging only on card-not-present invoices or for tickets above a threshold.

Alternatively, optimize debit and interchange first, negotiate markup, and reduce downgrades. Many Nashville merchants find they can save meaningfully without adding visible fees.

Q8) What simple steps can I take this month to cut costs?

Answer: Enable chip/contactless, fix batching cutoffs, turn on AVS/CVV, route debit optimally, and audit your pricing model against your real mix. Ask your MSP for a Durbin routing review and a Level 2/3 data checklist if you’re B2B. These changes typically deliver quick wins while you evaluate longer-term options like surcharging.

Conclusion

To control credit card fees for Nashville merchants, start with clarity: know the split between interchange, assessments, and markup; map your card mix and channels; and benchmark your effective rate by category. Prioritize debit optimization, downgrade prevention, and Level 2/3 data capture before considering surcharges.

If you do add a surcharge, configure technology to block debit, follow caps (Visa 3%; Mastercard and others up to 4% or your actual cost), notify your acquirer, and post compliant signage. Keep an eye on PCI DSS 4.0 timelines and debit-fee proposals so your setup stays future-proof.

For Nashville specifically, double-check sales-tax handling, especially with a common 9.75% combined rate, and tune your pricing model to your neighborhood and ticket size.

With these steps, Nashville merchants can turn payment acceptance from a frustrating line item into a disciplined, data-driven advantage—one that protects margins, improves customer experience, and scales smoothly as Music City keeps growing.